M&A Update: What We Saw in 2025 and How the Market Is Changing

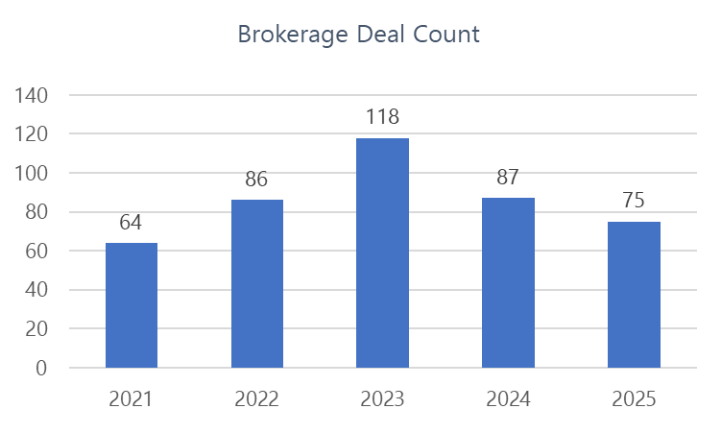

M&A activity in the Canadian insurance brokerage industry slowed in 2025, but the headline numbers only tell part of the story. 75 transactions were publicly announced during the year, the lowest level since 2022. This reflects a market that has become more selective, with fewer high-quality brokerages available and more discipline around what buyers are willing to pursue.

It is also important to note that many transactions are never publicly announced, particularly smaller acquisitions and tuck-ins. Based on our conversations across the market, overall activity is likely higher than public deal counts suggest.

What has not changed is the demand for strong brokerages. Owners of well-run businesses continue to attract interest, while others are finding the market more challenging than it was a couple of years ago.

Fewer Deals, More Selectivity

After several years of rapid consolidation, the supply of attractive brokerages has tightened. Many of the brokerages’ buyers most want to acquire have already sold, merged, or partnered with larger organizations. As a result, buyers are spending more time upfront, passing on more opportunities, and focusing their efforts where there is a clear strategic fit.

This has led to fewer announced deals, but not a quiet market. Buyers remain active, just more focused.

What has become increasingly clear is that owners are experiencing very different outcomes depending on how prepared their brokerage is when it comes to market.

Owners of well-run brokerages in 2025 typically saw multiple conversations, competitive interest, and flexibility around timing and structure. Other owners experienced something very different. Brokerages with heavier owner reliance, less clarity around growth, or more operational complexity often saw fewer buyers engage and less room to shape the outcome.

Who Is Buying?

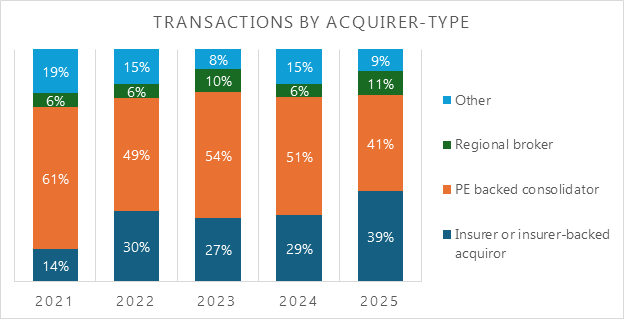

Private-equity-backed national consolidators continue to account for the largest share of transactions, in part because there are simply more of them, and acquisitions remain central to their growth. Just as importantly, these consolidators, both private-equity and insurance company-backed, have been the buyers willing to pay the highest prices, and they have largely been responsible for driving valuation levels across the industry.

This is reflected in public deal data. Almost all the publicly announced transactions included in industry deal counts are completed by national consolidators. There are relatively few publicly reported acquisitions by local or regional brokerages, even though those groups may still be active on a smaller and less visible basis.

Brokerlink, backed by Intact, stood out as the most active buyer of publicly announced deals in 2025.

We also saw new capital enter the industry, which is an important development looking ahead:

● Oracle RMS received new backing from Abry Partners

● Synex received investment from CDPQ and Ares

Both brokerages have clearly stated that acquisitions will play a key role in their future growth. While these investments did not immediately drive deal volume in 2025, they introduced new buyers with significant resources, which will influence competition going forward.

Another notable development was People Corporation’s acquisition of KASE Insurance, marking its move from group benefits into P&C. People Corp has been acquisitive in the benefits space for years, and this transaction adds another active buyer to the P&C landscape.

At the same time, several long-time consolidators appear to be slowing their pace slightly. They remain active but are buying fewer brokerages per year than at their peak. Integration capacity, internal focus, and discipline are now playing a larger role in decision-making.

Where Deals Are Being Publicly Announced

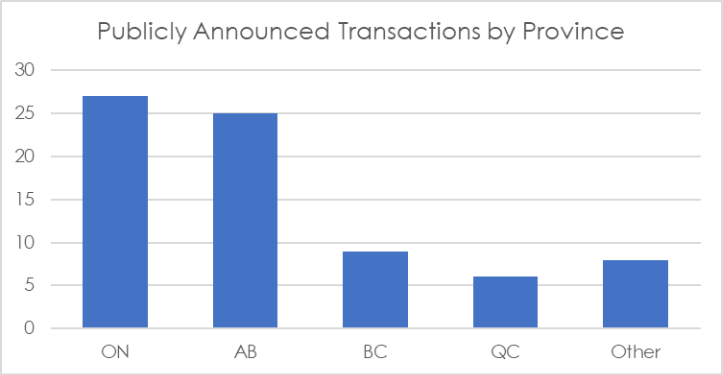

Publicly announced transactions continue to be concentrated in Ontario and Alberta. This largely reflects where national consolidators have focused their acquisition efforts, rather than a lack of activity in other provinces.

In markets where regional and local brokerages are more active buyers, transactions are more likely to occur quietly and are less frequently publicly disclosed. As a result, provincial deal counts tend to understate overall activity outside of Ontario and Alberta.

Valuations Remain Strong, but Outcomes Vary Widely

For owners of high-quality brokerages, 2025 was another strong year. Pricing held firm and, in some cases, improved. This strength is largely driven by scarcity. There are fewer brokerages today with strong leadership teams, clean operations, and clear growth stories than there were several years ago.

At the same time, the gap between outcomes has widened.

A key driver of this gap is who is interested in a given brokerage. National consolidators have consistently been the buyers willing to pay premium prices, and their participation, or lack thereof, has a significant impact on outcomes. When a brokerage attracts interest from one or more consolidators, pricing and deal flexibility tend to increase meaningfully. When consolidators are not interested, the buyer pool often shifts to regional or local brokerages, where pricing expectations are materially lower.

This is not a reflection of execution capability or intent. Regional and local brokerages simply cannot compete with the pricing levels national consolidators are able to support, given differences in scale, capital, and growth models.

One factor influencing this dynamic is how larger private-equity-backed brokerage platforms are valued relative to the acquisitions they pursue. These brokerages are under pressure to maintain overall value as they grow. They are often valued around 15–17x EBITDA at the platform level, which means most acquisitions need to be completed at lower multiples. While exceptions are made for particularly strong brokerages, including several transactions we were directly involved in, this reality has reinforced buyer selectivity and widened the gap between top-tier brokerages and the rest of the market.

One pattern we continue to see is that owners who engage the market on their own terms tend to have very different conversations than those who wait until a decision is forced by age, fatigue, or internal pressure. In the former case, owners retain flexibility around timing, role, and partner fit. In the latter, options tend to narrow quickly, even when the broader market is healthy.

Commercial and Personal Lines

Despite softening insurance markets, commercial brokerages remain in higher demand than personal-lines-focused firms, reflecting the complexity of the work and the strength of client relationships. However, softer markets are affecting financial performance, which means that while pricing frameworks remain strong, total transaction values can be impacted by lower recent earnings.

On the other hand, demand for smaller, personal-line-focused brokerages are weakening, even though hard market conditions are still driving growth in financial performance. Scale and strategic fit are becoming more important factors in determining buyer interest in this segment.

A Major Change at Year End

Late in 2025, Navacord announced its acquisition of Acera, expected to close in early 2026. This is a significant transaction that removes Acera as a potential buyer, effectively reducing the number of active bidders in the market.

On its own, fewer buyers would normally put pressure on outcomes. However, this change is occurring at the same time as new buyers are entering the space, which may offset that effect. The result is a market that looks different heading into 2026, but not meaningfully less competitive for strong brokerages.

Looking Ahead

The Canadian insurance brokerage M&A market continues to evolve. Buyers remain active and capital remains available, but outcomes are increasingly shaped by preparation, clarity, and fit rather than momentum alone.

For brokerage owners, the message is straightforward. Strong brokerages continue to attract interest and choice. Others are finding the market less forgiving than it once was.