What Actually Happens to Your Cap Table in a Down Round

If you’re a founder heading into a financing round where the valuation is lower than your last raise, you’re not alone. Down rounds have become a reality for many startups as valuations recalibrate from their 2021 to 2022 peaks.

In simple terms, a down round happens when a company raises new equity at a lower valuation than its previous round.

Most founders understand what that means at the headline level. Fewer understand what it actually does to the cap table once the round closes. It’s not a single event. It’s a cascade, and each step compounds on the last.

We recently completed a waterfall analysis for a Canadian startup raising a round at a pre-money valuation well below its prior rounds. The company had previously raised through preferred shares, SAFEs, and convertible notes at various stages. What we found is instructive for any founder heading into a similar situation.

In this post, we cover:

- How SAFEs, notes, anti-dilution, and option pools compound to reshape your cap table in a down round

- Why dilution doesn’t hit everyone equally

- Five things founders should consider before closing

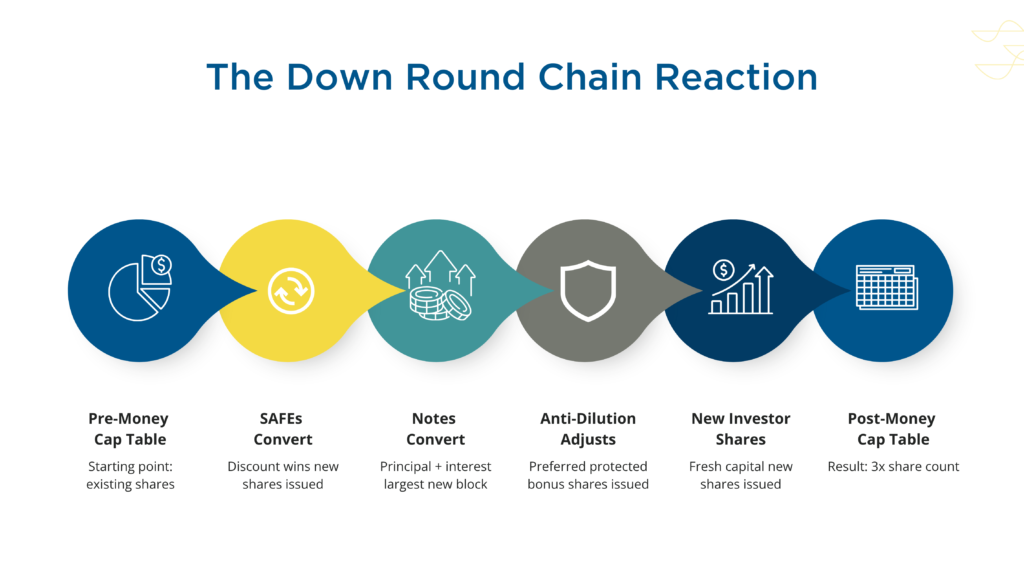

A Down Round Sets Off a Chain Reaction

When a new round prices below the last one, it doesn’t just create cheaper shares for new investors. It triggers a sequence of events across every convertible instrument, every preferred share class, and the option pool. Each event creates new shares and each new share dilutes existing holders.

Here’s the sequence:

SAFE conversion. SAFEs convert at the lower of two possible prices: one based on a discount to the round price, and one based on the SAFE’s valuation cap. In this case, the discount-based price came in well below the cap-based price, which meant SAFE holders ended up getting meaningfully more shares per dollar invested than new investors coming in at the round price. A 25% discount means SAFE holders pay 75% of the round price, so for every dollar invested, they receive a third more shares.

Convertible note conversion. Same discount-versus-cap logic, but notes also carry interest. In this case, accrued interest had added six figures to the total converting amount by close. All of it (principal and interest) converts at the discounted price. The note holders ended up with the single largest block of new shares in the entire cap table, larger even than the new investors.

Anti-dilution adjustment. Most preferred share classes include anti-dilution protection. This means that if the company later issues shares at a price below what the preferred holders originally paid, their conversion ratio gets adjusted. Each preferred share becomes convertible into more common shares than before. The most common form is weighted-average anti-dilution, which adjusts the ratio based on how many new shares are issued at the lower price relative to the total share count.

The preferred holders don’t pay anything extra for these additional shares. The dilution from them falls entirely on common shareholders who don’t have the same protection. In this case, both preferred classes had their conversion prices adjusted downward, entitling preferred holders to additional common shares upon conversion, at no extra cost.

Pre-money option pool expansion. Investors will sometimes require the company to expand its employee option pool as a condition of the round. When this expansion happens pre-money, the new shares get added to the share count before the round prices, which means they dilute existing holders rather than the incoming investors. It’s another lever that shifts dilution onto the cap table you already have.

One thing to keep in mind: These steps are all interdependent. The price per share depends on how many shares the SAFEs and notes convert into, but the number of conversion shares depends on the price per share. This is why down round cap tables are complex to model and worth having your advisors review independently.

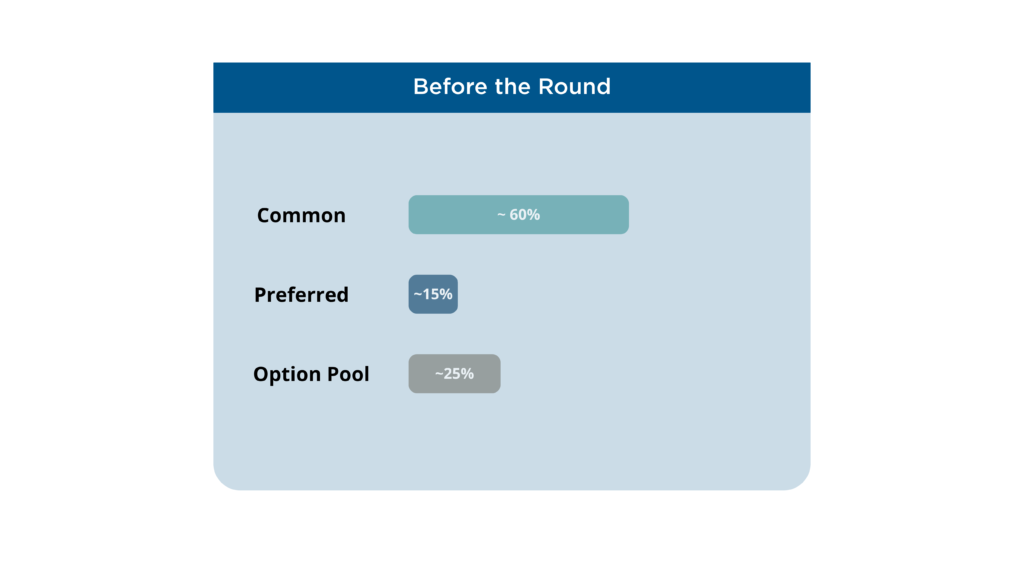

The Dilution Doesn’t Hit Everyone Equally

This is the part that surprises founders. A down round doesn’t spread the pain evenly. Every existing shareholder gets diluted, but common shareholders bear a disproportionate share. They have no anti-dilution protection, no discounted conversion, and no liquidation preference, so they absorb dilution from every direction.

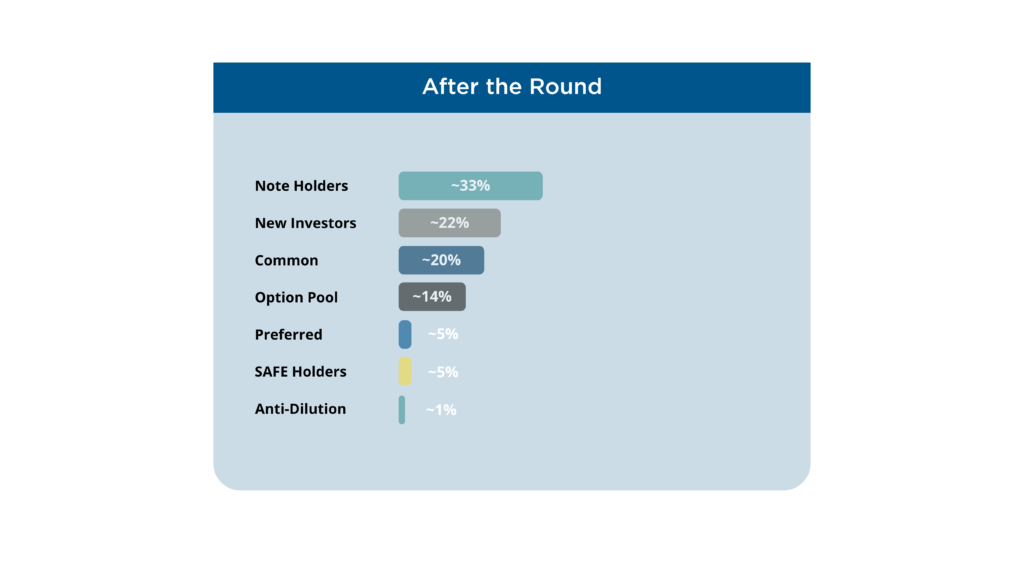

Shareholders who held only common shares saw their ownership drop by as much as two-thirds. Meanwhile, shareholders who also held convertible instruments or preferred shares were partially or fully offset by their conversion shares and anti-dilution adjustments. Same transaction, completely different outcomes depending on what protections you have.

The largest institutional investor combined their preferred shares, anti-dilution adjustment, and note conversion to become the single biggest post-round holder. Note holders as a group went from zero equity (their instruments were still debt) to owning roughly a third of the company.

Lastly, anyone holding options with an exercise price above the new round price saw their options go underwater when the round closed. In this case, some option holders had exercise prices more than double the new price per share.

Five Things to Consider Before You Close

Based on what we see across Canadian startup financings, here are the key areas founders should be thinking about heading into a down round:

1. Understand how your conversion prices work. For both SAFEs and convertible notes, the conversion price is the lower of the discount-based price and the cap-based price. In a down round, the discount often wins. In an up round, it’s typically the cap. Make sure you understand which applies to each instrument in your cap table and what that means for the number of shares being issued.

2. Don’t overlook accrued interest on convertible notes. Make sure you account for the specific terms of each note and how many you have. In our engagement, accrued interest across all notes added six figures to the total converting amount. That’s six figures converting into equity at the discounted price.

3. Know what triggers your anti-dilution provisions. Not every share issuance triggers an anti-dilution adjustment. Most articles of incorporation define certain issuances as ‘Exempted Securities’, meaning they don’t count. Whether SAFE and note conversions are considered exempted can change the anti-dilution outcome. This is a legal question and worth confirming with legal counsel.

4. Pay attention to the option pool expansion. New investors sometimes require the company to expand its employee option pool before the round closes. When this expansion happens pre-money, the dilution from those new options falls entirely on existing shareholders – not on the incoming investors. Understand how large the expansion is and recognize that it’s another source of dilution on top of everything else.

5. Model any warrants. If warrants are being issued as part of the round, their terms need to be understood: exercise price, quantity, share class, and whether they’re included in the fully diluted count. We’ve seen founders treat warrants as immaterial, only to find they triggered additional anti-dilution adjustments or changed the price per share calculation.

The Bigger Picture

A down round is a survival tool. It keeps the company alive when the market doesn’t support the prior valuation.

But the mechanics are complex and the stakes are high. Ownership percentages can shift by double digits in a single transaction. The difference between getting the waterfall model right and getting it wrong can materially change how value is attributed across shareholders.

If you’re heading into a down round, understand what’s happening to your cap table before the round closes, not after. Have your advisors build or review the waterfall model independently. Ask about anti-dilution methodology, conversion pricing, and the qualified financing threshold. The math matters.

We Help Founders Get Clarity on the Numbers

Whether you’re modeling a new raise, reviewing a term sheet, or trying to understand how your cap table looks post-close, our Technology and Advisory team works with Canadian startups at every stage. If you’re heading into a down round or reviewing a term sheet, reach out to our team for an independent cap table review.